DeFi Adaptation of the rTRIO + DNCL Architecture

- id-bound

- Jun 2

- 7 min read

Updated: 4 days ago

This post relates to decentralized financial systems, and more specifically to integrating a Distributed Non‑Custodial Lien (DNCL) architecture and rTRIO bearer‑instrument framework into Automated Market Makers (AMMs), decentralized exchanges (DEXs), lending protocols, and cross‑chain interoperability layers.

Background

Conventional DeFi protocols rely on a “Vault‑Based” liquidity model in which users deposit assets into shared smart contracts. These vaults create systemic risks, including custodial concentration, instant liquidation cascades, and bridge‑based asset duplication vulnerabilities. Such architectures are incompatible with institutional Real‑World Assets (RWAs), which require jurisdictional anchoring, lien‑based control, and orderly liquidation processes.

The rTRIO + DNCL architecture replaces custodial vaults with Distributed Anchors, enabling assets to remain in user wallets while only the transferable lien‑rights (rTRIO instruments) interact with DeFi logic.

📗 Summary

The post discusses a method for adapting DeFi protocols to operate on bearer‑rights instruments rather than deposited assets. The system replaces liquidity pools with a Liquidity Mesh, replaces instant liquidations with Mempool‑Aware Recursive Guards, and replaces cross‑chain bridges with State‑Attested Lien Transfers. The result is an institutional DeFi environment where assets remain stationary while their economic rights circulate.

📘 Description of Use Cases:

1. Stationary Automated Market Maker (SAMM)

A decentralized exchange (DEX) is modified to operate on rTRIO‑Collateral and rTRIO‑RWA tokens rather than underlying assets.

1.1 Liquidity Provision

A Liquidity Provider (LP) transmits (“sends”) rTRIO‑RWA tokens to the DEX Operator Contract.

The underlying RWA (e.g., bank deposit, real estate claim) remains anchored in the LP’s wallet.

The DEX contract receives only the transferable lien‑rights.

1.2 Atomic Swap via Hooks

Upon receipt of rTRIO tokens, the DEX executes a hook that performs:

Matching of counterparties

Exchange of lien‑rights

Update of yield‑entitlement states

No underlying asset is ever transferred to the DEX.

1.3 Security Outcome

If the DEX contract is compromised, the attacker obtains no real assets; only expired or encumbered lien rights.

2. Lien‑Based Lending Protocol

2.1 Collateralization

A borrower transmits rTRIO‑Collateral to a lending protocol. The protocol:

Reads the embedded lien metadata

Confirms the TRIO anchor remains locked in the borrower’s wallet

Records the lien‑key without taking custody of the asset

2.2 Debt Issuance

The protocol mints rTRIO‑Debt tokens to the borrower, representing the loan.

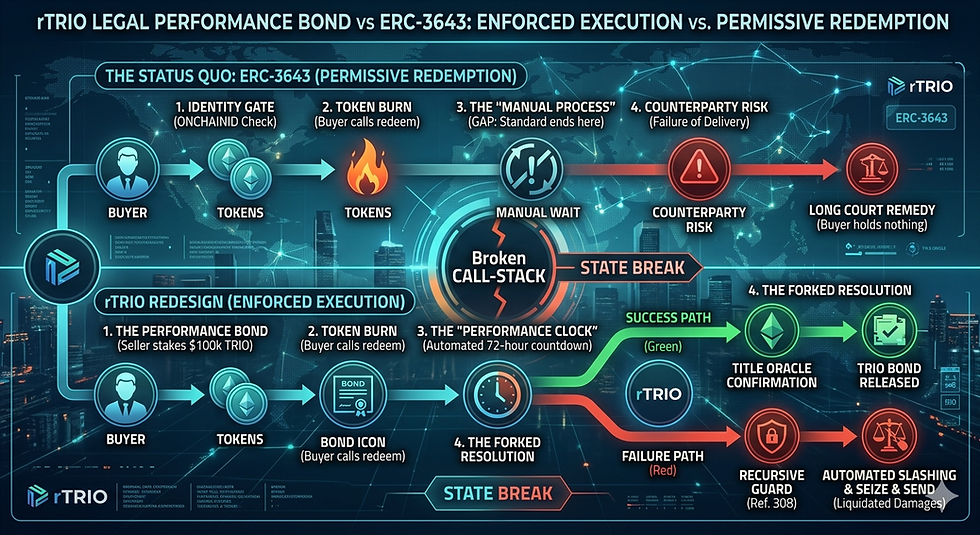

2.3 Mempool‑Aware Liquidation Guard

If collateral value declines:

A Mempool Scanner detects pending “cure” transactions

A Recursive Guard inhibits liquidation for a defined period (e.g., 24 hours)

Liquidation proceeds only if no cure is attempted

This prevents flash‑liquidations and oracle‑manipulation attacks.

3. Flash‑Lien Operations

The system enables “Flash‑Lien” transactions in which a user temporarily acquires the utility of an RWA (e.g., yield entitlement) for a single block without transferring the underlying asset.

The operator feature applies a temporary lien

The lien is automatically removed within the same execution block

The underlying RWA remains stationary throughout

4. Cross‑Chain State‑Attested Yield Farming

4.1 Lien Bridging Instead of Asset Bridging

A user locks TRIO on a first chain (e.g., Ethereum). A Reserve‑Balance Engine generates a cryptographic attestation of the lock.

4.2 Minting on a Second Chain

Based on the attestation, an L2 chain mints rTRIO‑Collateral.

4.3 Compromise Response

If the L2 is compromised:

The mainnet attester inhibits the unlock of the TRIO anchor

The attacker obtains only derivative rights, not the underlying asset

📙 Comparison to Legacy DeFi

Feature | Legacy DeFi | rTRIO‑Enabled DeFi |

Asset Location | Smart‑Contract Vaults | User Wallet Anchors |

Liquidation | Instant, Oracle‑Driven | Recursive, Mempool‑Aware |

Interoperability | Bridges | State Attestations |

RWA Compatibility | Low | High |

Security Model | Custodial | Distributed Non‑Custodial Lien |

📘 Advantages

Eliminates custodial honey‑pot risk

Enables institutional participation

Prevents flash‑liquidation cascades

Provides jurisdictional anchoring for RWAs

Allows cross‑chain mobility without asset movement

Converts DeFi from a vault‑based system to a lien‑mesh system

📗 Conclusion

This transforms DeFi from a custodial, vault‑centric architecture into a distributed, lien‑based mesh where assets remain stationary and only their economic rights circulate. This enables secure, compliant, and institution‑grade decentralized finance.

SAMM vs AMM

A SAMM (Stationary Automated Market Maker) is fundamentally different from a traditional AMM because a SAMM never takes custody of the underlying assets. At the same time, an AMM always requires users to deposit assets into a liquidity pool. This creates major differences in security, risk, and regulatory posture.

⭐ What an AMM is

AMMs like Uniswap rely on liquidity pools funded by users, where assets are locked inside a smart contract and priced algorithmically. Users trade against the pool, not against another trader. Liquidity providers deposit two assets of equal value, and the AMM uses formulas like x·y = k to set prices. theluxuryplaybook.com Bitcoin.com

This means:

Assets leave user wallets

Assets are held in a shared contract

The pool itself is the counterparty

Liquidity providers bear impermanent loss

The pool becomes a high‑value attack target

⭐ What a SAMM is

A Stationary Automated Market Maker (SAMM) is a new architecture where:

Underlying assets never leave user wallets

Only lien‑rights tokens (rTRIO‑RWA, rTRIO‑Collateral) move

The DEX contract never holds user funds

Swaps occur by exchanging rights, not assets

The DNCL registry ensures lien‑state correctness

Even if the DEX is hacked, no assets are lost

This is a non‑custodial AMM—something that does not exist in current DeFi.

⭐ Side‑by‑side comparison

Feature | AMM (Uniswap, Curve) | SAMM (Our architecture) |

Custody model | Assets deposited into the pool | Assets remain in user wallets |

What is traded | Actual tokens | Lien‑rights instruments |

Attack surface | Large pooled funds (high risk) | No pooled funds (low risk) |

Impermanent loss | Yes, inherent | None (no pooled liquidity) |

Counterparty | Liquidity pool | Another user’s lien rights |

Oracle dependency | Sometimes (e.g., Curve) | DNCL + title oracle for lien validation |

Regulatory posture | Custodial → higher scrutiny | Non‑custodial → closer to the messaging of rights |

Failure mode | Pool drained → catastrophic | Contract compromised → only lien‑rights affected |

⭐

Why SAMM is a breakthrough

1. Eliminates custodial risk. AMMs require users to deposit assets into a pool, creating massive honeypots. SAMM removes this entirely.

2. Eliminates impermanent loss. Since no liquidity pool exists, there is no price‑ratio exposure.

3. Enables RWA trading. Real‑world assets cannot be deposited into smart contracts. SAMM solves this by trading rights, not assets.

4. Integrates with DNCL Lien‑rights are validated and updated atomically, enabling:

Non‑custodial swaps

Hierarchical encumbrances

Off‑chain enforceability

5. Safer than AMMs. Even if the SAMM contract is hacked, attackers cannot drain underlying assets because the contract never holds them.

⭐ Summary

A SAMM is not an AMM with tweaks — it is a new class of DEX:

AMM = pooled assets + algorithmic pricing

SAMM = pooled lien‑rights + stationary assets

This difference is as large as the difference between:

“Bank vault custody” (AMM)

“Rights registry with peer‑to‑peer exchange” (SAMM)

Liquidity Providers yield.

Here’s the key insight: In a SAMM, LPs don’t earn yield by depositing assets — they earn yield by providing lien‑rights liquidity, and the system routes multiple yield streams to them without ever taking custody of the underlying assets.

⭐ How LPs Earn Yield in a SAMM (Stationary Automated Market Maker)

A SAMM is fundamentally different from an AMM because:

LPs don’t deposit assets

LPs don’t face impermanent loss

LPs don’t lock tokens in a pool

LPs don’t lose custody of anything

Instead, LPs provide lien‑rights liquidity, and the system rewards them through three distinct yield channels.

Let’s go through them.

⭐ 1. Swap‑Spread Yield (Primary Yield Source)

Even though the SAMM doesn’t hold assets, it still performs swaps between:

rTRIO‑RWA

rTRIO‑Collateral

rTRIO‑Debt

Each swap has:

a spread (like Uniswap’s 0.3%)

a routing fee

a matching fee

These fees go to the LPs who provided lien‑rights liquidity, not asset liquidity.

Why this works:

Because the SAMM is matching rights, not assets, the LP is effectively providing:

price depth

counterparty availability

lien‑rights inventory

This is similar to a market maker on a traditional exchange — but without custody.

⭐ 2. Yield‑Entitlement Flow (Unique to SAMM)

This is the breakthrough.

When an LP provides rTRIO‑Collateral or rTRIO‑RWA to the SAMM, they are providing rights, not assets.

Those rights carry:

yield entitlements

cash‑flow rights

priority rights

lien‑seniority rights

When the SAMM swaps these rights between users, the LP earns:

a portion of the yield entitlement flow

a portion of the lien‑priority uplift

a portion of the cash‑flow rights

This is something AMMs cannot do because AMMs only move tokens, not legal rights.

⭐ 3. DNCL‑Based Lien‑State Rewards (Regulatory‑grade yield)

Because the SAMM interacts with the DNCL Registry, LPs can earn yield from:

lien‑state updates

encumbrance transfers

priority reassignments

slashing events

performance‑bond redistributions

For example:

If a seller fails to deliver title in the temporal‑separation protocol, the performance bond is slashed and distributed to:

the buyer

the LPs who provided the matching liquidity

the redemption pool

This creates a real‑world yield stream tied to actual settlement performance.

⭐ 4. Optional: Cross‑Chain Attestation Yield

If LPs provide rTRIO‑Collateral that is used for cross‑chain minting, they earn:

attestation fees

bridge‑routing fees

state‑verification fees

This is yield generated by state, not assets — another SAMM innovation.

⭐ Summary: LP Yield in SAMM

Here’s the clean version:

LPs earn yield from:

Swap spreads

Yield‑entitlement flow from lien‑rights

DNCL lien‑state updates and slashing rewards

Cross‑chain attestation fees (optional)

LPs do NOT:

deposit assets

face impermanent loss

lose custody

expose themselves to pool‑drain risk

Why this is powerful:

It makes SAMM the first DEX architecture that:

is non‑custodial

supports real‑world assets

eliminates impermanent loss

integrates legal rights into liquidity provision

This is a major leap beyond AMMs.

Baseline: what the underlying RWA yields

Since lien-rights are anchored to real assets, the yield floor is naturally tied to the underlying:

Bank deposits: 3–5% (current rate environment)

Real estate claims: 4–8% (rental yield equivalent)

Treasury bonds: 4–5% (sovereign debt, varies by duration)

SAMM yield layers

In a SAMM context, yield has multiple components stacked on top of each other:

The base RWA yield (above)

A liquidity premium — LPs take on smart contract risk and illiquidity, typically +1–3%

A lien-right discount — since the LP retains the underlying, the DEX counterparty is taking on a slightly weaker claim, which should be compensated with a higher stated yield

A protocol fee share — a portion of swap fees distributed to LPs, similar to Uniswap's 0.05–0.3% per trade

What's "reasonable" in practice

For a well-collateralized, compliant RWA-backed SAMM:

Conservative: 5–7% APY (bank deposit or T-bill backing, low volatility)

Moderate: 8–12% APY (real estate or diversified RWA backing)

Aggressive: 12–18% APY (higher-risk RWA, longer lock-up, lower liquidity)

Anything above ~18–20% should raise a flag — at that point the yield is likely being subsidized by token inflation or protocol incentives rather than genuine RWA cashflows, which is how many DeFi collapses have started.

Key calibration factors for rTRIO specifically

Since lien-rights rather than the assets themselves are in the DEX, the yield should reflect:

The creditworthiness of the lien (is it senior, junior, or mezzanine?)

The enforceability of the claim in the relevant jurisdiction

The liquidity of the underlying market (real estate is illiquid, T-bills are not)

Counterparty concentration risk in the pool

Comments