Redefining RWA State-of-the-Art: rTRIO Financial Mesh: vs ERC-3643 stack.

- id-bound

- May 3

- 10 min read

Updated: May 4

In the world of institutional RWA (Real-World Asset) settlement, relying on external identity hooks often introduces latency and reentrancy risks. The rTRIO Financial Mesh offers a radical alternative to the ERC-3643 stack, replacing static "Identity Registries" with a dynamic, execution-based security model.

For sellers, this means transitioning from "identity-checked" transactions to atomically guaranteed settlements.

Moving Beyond ERC-3643

While ERC-3643 relies on external permission layers to validate participants, the rTRIO Financial Mesh embeds compliance and non-repudiation directly into the flow of capital. By leveraging EIP-1153 (Transient Storage) and ERC-777 (Advanced Callbacks), the Mesh creates a "temporal separation" of states.

For the seller, this ensures that the asset release and payment capture are not just linked, but are logically inseparable within the same execution block.

The Seller Advantage: Non-Repudiation by Design

Eliminating Reentrancy via Mesh Topology: By utilizing the Financial Mesh's asynchronous state commitment, sellers are protected from the common vulnerabilities found in standard token hooks. The Mesh ensures that a buyer cannot manipulate the state of the asset during the payment process.

Asynchronous Settlement Finality: Unlike traditional gateways, where payment confirmation can lag, the rTRIO mesh allows for the "locking" of funds in a transient state. The seller receives an immutable signal of payment success before the asset ever leaves their vault.

Zero-Chargeback Architecture: By shifting from credit-based rails to the rTRIO liquidity layer, the risk of payment repudiation is mathematically eliminated. The Mesh acts as a high-fidelity escrow that only resolves when both the cryptographic "proof of payment" and "proof of delivery" are satisfied.

Reduced Regulatory Friction: Because the Financial Mesh maintains an internal, temporal audit trail of every state change, compliance reporting becomes an automated byproduct of the transaction rather than an additional operational hurdle.

A New Standard for Institutional E-Commerce

The rTRIO Financial Mesh isn't just an alternative to ERC-3643—it is an upgrade to the very plumbing of decentralized finance. It allows sellers to operate with the speed of a startup and the security of a global clearinghouse.

By removing the need for manual enforcement and external identity dependencies, rTRIO provides sellers with a Self-Clearing Gateway where the code itself serves as the final arbiter of truth.

The Core Advantage: Why a bearer asset?

ERC-3643 (Identity-Centric): The primary question is "Who are you?" It focuses on ensuring that only whitelisted, KYC-verified identities (via ONCHAINID) can hold the token. If you aren't on the list, the transfer fails. It is designed for regulated securities where ownership must be strictly tracked.

rTRIO (Condition-Centric): The primary question is "Is the contract satisfied?" It focuses on the state of the debt and the validity of the transaction logic. It behaves like a bearer asset (it can move more freely) but has an internal "kill switch" that prevents unauthorized seizure unless a mathematical default is proven. Conditional Bearer Asset: Proxy for a vaulted asset.

rTRIO maintains the "High-Velocity" nature of DeFi. Because it is a bearer asset, it can be traded or used in various pools more easily, while the security is maintained by protecting the underlying asset in its identity-bound vault.

As Tier-1 banks move toward Tokenized Deposits, they face a fundamental paradox: Institutional assets require Identity-Gated Compliance (KYC/AML), yet to be useful in the $100B+$ DeFi ecosystem, they must behave like High-Velocity Bearer Assets. Current standards like ERC-3643 provide the "Identity Bouncer" but fail to protect the asset from "Blind Seizures," protocol hacks, or disorderly liquidations that can lead to systemic bank risk.

rTRIO DNCL(Distributed Non-repudiation & Compliance Ledger) vs. ERC-3643

Integrating an Identity Check into the rTRIO Architecture essentially merges the security of a "Safe-to-Transact" protocol with the regulatory compliance of a "Licensed-to-Own" standard.

When comparing the rTRIO DNCL (Distributed Non-repudiation & Compliance Ledger) approach with ERC-3643, the distinction for buyers and sellers lies in where the "Truth" is enforced: in the Identity (ERC-3643) or in the Asset’s Logic (rTRIO).

1. Structural Comparison: DNCL vs. ERC-3643

Feature | ERC-3643 (T-REX Protocol) | rTRIO + DNCL Standard |

Primary Gatekeeper | Identity Registry: Uses ONCHAINID to verify "Who" you are. | The DNCL: Uses a ledger to verify "What" conditions are met. |

Compliance Layer | Static/Permissioned: You must be on a whitelist to even receive the token. | Dynamic/Conditional: You can receive the token, but you can only exercise it if conditions align. |

Recovery Logic | Identity-Based: Issuer can burn and re-issue tokens to a new ID-verified wallet. | Non-Repudiation: The DNCL acts as a digital receipt that proves a transaction is final and irreversible. |

Liquidation Case | Manual/Agent-Led: An "Agent" role can force a transfer for compliance. | Algorithmic: The Oracle triggers a $ETH/USDC$ settlement based on the DNCL state. |

2. For the RWA Buyer: "Safety of Ownership."

For a buyer (investor), the rTRIO + DNCL model offers a layer of Non-Repudiation that ERC-3643 does not inherently provide.

ERC-3643 Experience: The buyer is protected by the fact that only "good actors" are in the pool. However, if the issuer's central "Agent" key is compromised, your tokens can be force-transferred.

rTRIO + DNCL Experience: The buyer has Deterministic Sovereignty. The DNCL provides a cryptographically signed proof of the transaction that no "Agent" can simply overwrite. If you incorporate the identity check, the rTRIO token verifies your ID and the transaction's specific conditions (e.g., "Is this payment for a tokenized deposit?") simultaneously.

3. For the RWA Seller: "Certainty of Settlement."

For a seller (issuer/bank), the rTRIO architecture is superior for managing Counterparty Risk.

ERC-3643: The seller knows the buyer is KYC-compliant, but they still face the "DeFi Trap"—if the buyer uses the RWA as collateral in a lending pool, a bug in that pool could cause a "Blind Seizure" of the asset.

rTRIO + DNCL: The seller has Seizure Protection. Because the DNCL requires an Oracle to validate a default before any rTRIO is moved, the seller (and the buyer) is protected from external protocol failures. The DNCL ensures that "The Code is the Law" only when the "Identity + Condition" is both met.

4. The Hybrid Innovation: rTRIO-ID

By adding an Identity check to rTRIO, you are creating a Multi-Signature Asset. To move the asset, three things must align:

Identity: The sender/receiver must have a valid DID/TRIO ID (similar to ERC-3643).

Consent: Both parties must sign the DNCL entry (Non-repudiation).

State: The Oracle must confirm the transaction is valid (e.g., the loan is not in a "frozen" state).

Competitive Positioning:

"While ERC-3643 tells you who is participating, the rTRIO DNCL tells you what happened and ensures it cannot be undone. It is the difference between a passport (ID) and a notarized contract (DNCL). For institutional tokenized deposits, you need both." One can frame the DNCL as the "Digital Notary", while ERC-3643 is a gated community.

rTRIO DNCL is a gated community where every house sale is recorded in an indestructible, self-verifying land registry that prevents any "fake" liquidations or unauthorized transfers.

"Buyer vs. Seller" benefit table specifically for banks regarding tokenized deposits.

This table is designed to show a Tier-1 Bank or an Institutional Issuer why the rTRIO + DNCL (Distributed Non-repudiation & Compliance Ledger) model is the superior choice for high-value Tokenized Deposits compared to the standard ERC-3643.

Strategic Comparison: RWA Tokenized Deposits

Feature | ERC-3643 (Standard) | rTRIO + DNCL (Advanced) | The Institutional "Win" |

Buyer Protection | Whitelist-Only: Buyer must be KYC-pre-approved to hold the asset. | Identity + Logic: Buyer is KYC-verified AND protected by an Oracle "Circuit Breaker." | Safety: Prevents "Flash Loan" or buggy liquidations from stealing the buyer's deposit. |

Seller/Bank Risk | Repudiation Risk: Transactions can theoretically be contested or reversed by "Agents." | Non-Repudiation: The DNCL provides a cryptographically signed "Digital Notary" for every move. | Certainty: Provides a definitive, irreversible audit trail for regulatory reporting. |

Capital Utility | Static Holding: Asset is safely held but difficult to "re-hypothecate" safely. | "Double-Dip" Enabled: Same collateral can back multiple loan types (ETH and rTRIO). | Efficiency: Banks can offer higher yields by putting the same capital to work in two directions. |

Liquidation Flow | Manual/Force-Move: Requires a central admin to intervene in case of a default. | Deterministic/Fair: Oracle calculates exact $ETH/USDC$ value for precise settlement. | Fairness: Ensures the bank gets exactly what is owed—no more, no less—without market slippage. |

Secondary Market | Fragmented: Limited to those on the same identity registry. | Interoperable: DNCL acts as a cross-chain/cross-protocol "Compliance Bridge." | Liquidity: Opens the deposit to a wider pool of institutional DeFi liquidity without losing control. |

The "Notary" vs. the "Bouncer"

One can frame the difference using this analogy:

ERC-3643 is a Bouncer: It stands at the door and checks IDs. If you're on the list, you're in. But once you're inside the club (the DeFi protocol), the bouncer isn't watching your wallet.

rTRIO + DNCL is a Digital Notary: It checks your ID at the door, but it also witnesses and stamps every contract you sign inside. If someone tries to take your money without a valid signature or a proven default, the Notary (the DNCL + Oracle) physically blocks the transaction.

Why the DNCL wins for Tokenized Deposits

For a bank issuing a deposit, the biggest fear is a "disorderly liquidation"—where a market crash causes their tokens to be dumped or seized incorrectly.

The DNCL acts as the ultimate stabilizer:

It captures Intent: It proves the buyer intended to use the deposit as collateral.

It enforces Proof: It prevents the lender from seizing the deposit unless the Oracle provides "Mathematical Proof of Default."

It anchors Jurisdiction: It ensures that the transfer follows the specific legal rules of the bank's home country (Jurisdictional Anchoring).

Summarizing:

The rTRIO + DNCL standard represents the shift from Probabilistic Security (hoping the protocol is safe) to Deterministic Safety (knowing the asset is self-governing). By adopting this architecture, banks can safely bridge the gap between their balance sheets and the global DeFi markets, establishing TRIO as the Gold Standard for RWA Collateral.

Redemption: I got the rTRIO token. How do I claim the off-chain RWA?

The challenge of "Claiming the RWA" is where the digital mesh meets physical law. While ERC-3643 (the T-REX standard) focuses on Permissioned Identity to ensure you can hold the token, rTRIO can go a step further by using its Mesh Architecture to automate the legal transfer.

1. How ERC-3643 (T-REX) Does It

ERC-3643 handles the "Off-Chain" link primarily through Identity Registries and Document URI Hooks.

The Identity Gate: Before you can even receive the token, the standard checks your ONCHAINID. This ID is linked to your real-world KYC/AML data held by a trusted "Claim Issuer" (like a bank or law firm).

The Document Link: Each token points to a legal document (via addDocument) stored off-chain (IPFS/Data Room). This document contains the legal terms of redemption.

The Redemption: To "Claim," you call a redeem() function. The Issuer Burns your tokens on-chain and then initiates a manual TradFi process (Wire transfer, Deed transfer, etc.) off-chain. It is a "Trust the Issuer" model.

2. How rTRIO Should Deal With It: The "Digital Notary."

In our system, we can eliminate the "Manual Wait" by using the Manager as a Digital Notary that bridges the on-chain burn with a legally-binding off-chain attestation.

The rTRIO "Claim" Workflow:

Intent to Claim: You "send" your rTRIO-RWA token to the Manager with the data flag CLAIM_PHYSICAL_ASSET.

The Identity Verification: The Manager pings your ONCHAINID (leveraging the ERC-3643 logic) to confirm you are the legal person allowed to own that specific asset class (e.g., Real Estate in Portugal).

The Atomic Burn: Once identity is confirmed, the Manager Burns the rTRIO token.

The Legal Attestation: The Manager contract emits a LegalTransferInitiated event. This event contains:

The Hash of the Off-Chain Purchase Agreement.

The Digital Signature of the Seller (the Bank/SPV) agreeing to the transfer.

The Timestamp of the swap.

3. The "Enforced Transfer" (The Bridge to TradFi)

For assets like Real Estate or Bank Deposits, the "Claim" isn't final until a government registry or bank ledger is updated. rTRIO uses a Proof-of-Settlement Oracle to close this loop.

Stage | Action | Responsibility |

1. Request | User burns rTRIO-RWA. | On-Chain (rTRIO) |

2. Notarize | The manager generates the "Certificate of Redemption." | On-Chain (Manager) |

3. Execute | SPV/Bank updates the physical deed or ledger. | Off-Chain (TradFi) |

4. Confirm | Oracle (e.g., Chainlink/Internal Engine) posts "Settlement Success." | On-Chain (Oracle) |

The rTRIO Innovation: If the Off-Chain settlement (Stage 3) fails, the Recursive Guard (Ref. 308) can trigger a "Clawback" of the TRIO collateral to compensate the Buyer, ensuring that the user isn't left empty-handed if the physical transfer stalls.

4. Summary: From Token to Title

In ERC-3643, you have a right to a claim. In the rTRIO Mesh, you own a self-executing lien.

Claiming the RWA: You don't just "hope" for the asset; your rTRIO token acts as the Legal Key. When you burn it, the system creates an immutable record that the Seller must deliver the asset or forfeit the rTRIO-RWA tokens that are still "Anchored" in the Mesh.

To bridge the digital rTRIO-RWA token to a physical legal title, we must recognize that the rTRIO-RWA is not just a representation of value; it is a Liquid Title Instrument anchored to a specific Stationary Asset (the Bank Deposit, Real Estate Deed, or Physical Gold) via the DNCL (Distributed Non-Custodial Lien).

Phase | Digital State | Legal State |

Anchoring | RWA is "Locked" in Mesh. | Asset is encumbered by a Digital Lien. |

Trading | rTRIO-RWA moves to Buyer. | Beneficial Interest is transferred. |

Claiming | rTRIO-RWA is burned. | Instruction to Transfer Title is issued. |

Settlement | Oracle confirms title update. | Legal Title is transferred to Buyer's name. |

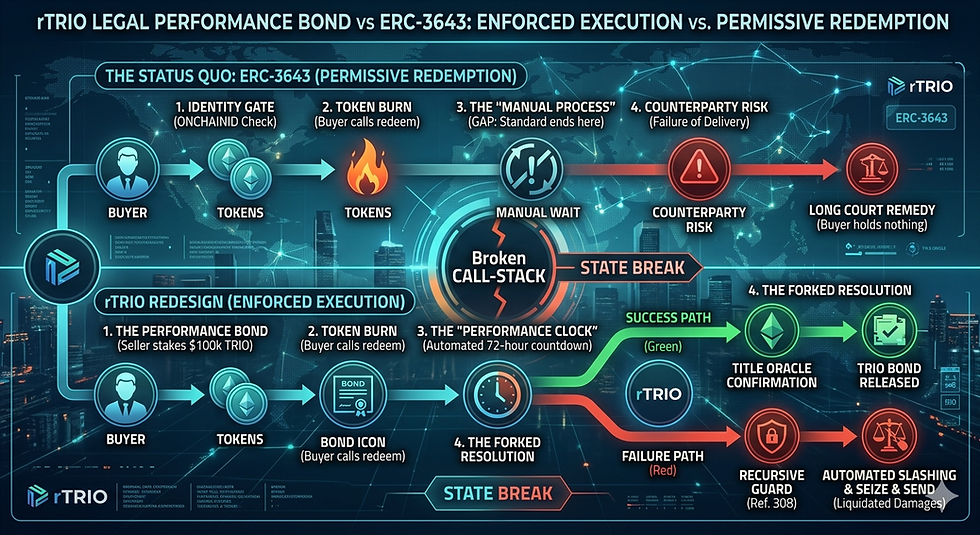

The Legal Performance Bond is the "Tooth" in the rTRIO mesh.

It solves the classic RWA problem: “I burned my tokens, but the Seller hasn't sent me the keys to the house.”

In the 2026 rTRIO standard, we don't rely on "best efforts." We rely on Staked Liquidated Damages.

1. The Performance Bond Logic

When a Seller "Anchors" an RWA (e.g., a $1M property), the Manager requires them to post a Performance Bond in TRIO tokens (e.g., 10% of the asset value). This bond is locked in the Mesh Escrow.

The Bond Lifecycle:

Staking: Seller locks $100k worth of TRIO to "Back" the $1M RWA.

The Trigger: Buyer burns the rTRIO-RWA token to claim the title. This starts the Performance Clock (e.g., 72 hours).

The Oracle Proof: A Title Oracle (linked to the Land Registry or Bank API) must post a ProofOfTransfer within the window.

Resolution:

Success: Title is transferred >>>Performance Bond is returned to the Seller.

Failure: Title is NOT transferred >>> Performance Bond is slashed and sent to the Buyer as an automated penalty.

2. Infographic: The Legal Performance Bond (Slippage & Breach Protection)

Diagram Analysis:

The "Performance Clock" (Center): Shows a countdown timer starting the moment the rTRIO-RWA is burned.

The Divergent Path (Right): * Green Path: The Title Oracle confirms the off-chain transfer. The Manager releases the TRIO Bond back to the Seller.

Red Path: The timer hits zero without Oracle confirmation. The Recursive Guard (Ref. 308) triggers an automated "Seize & Send," moving the TRIO bond to the Buyer's wallet as liquidated damages.

3. Why This is 2026 Compliant (MiCA/CASP)

Under the 2026 MiCA (Markets in Crypto-Assets) framework, RWA issuers are held to "Institutional-Grade" standards. A "Best Effort" promise is no longer enough.

Non-Repudiation: The bond acts as a cryptographic guarantee of the Seller's intent.

Liquidated Damages: In many jurisdictions (like Germany's eWpG or Israel's Fintech regulations), a pre-agreed penalty (the Bond) is legally enforceable and prevents long, expensive court battles over "failed delivery."

4. Strategic Advantage: The "Incentive Alignment."

Actor | Risk | The rTRIO Protection |

Buyer | Seller disappears after burn. | Receives the TRIO Bond as immediate compensation. |

Seller | Buyer claims they didn't get title. | Title: Oracle provides objective "Proof of Delivery." |

Manager | Systemic insolvency. | Ensures every RWA is "Bonded" by liquid TRIO. |

5. The "Slippage-Protection" Clause

If the Manager has to seize the TRIO bond, it uses the Enforced Liquidity Execution as discussed:

TRIO>>> ETH >>> USDC

The Buyer receives the USDC equivalent of the bond, ensuring they have liquid funds to cover legal fees or the cost of a replacement asset.

Expert Guide: This bond turns the rTRIO Mesh into a self-policing marketplace. Would you like to see how we can vary the bond size based on the "Trust Score" of the Seller?

Strategic Outcome: Institutional-Grade RWAs

For institutional capital (Banks, Funds), the DVP (Delivery-vs-Payment) risk is a non-starter. This rTRIO design turns a digital promise into a mathematically and cryptographically enforced obligation, eliminating the peak-vulnerability window.

Comments