TRIO Alternative Payments- the Big Picture.

- id-bound

- Jan 12, 2024

- 3 min read

Updated: Mar 26, 2024

We will discuss here the Economics of E-commerce with state-of-the-art cybersecurity, and the use case for alternative payments.

Internet E-Commerce is huge. So is the financial crime around it:

Problem #1: Theft.

Theft in the context of the Internet often involves unauthorized access or taking control of assets, such as money, without the owner's consent. The financial impact of theft on the internet is substantial. Reports and studies suggest that global losses due to cyber theft can range from tens of billions to hundreds of billions of dollars annually.

Problem #2: Fraud.

Fraud involves deceptive practices designed to gain an advantage unlawfully, typically for financial gain. Fraudulent activities on the internet contribute significantly to financial losses. Estimates for the global cost of online fraud often range from tens of billions to over a hundred billion dollars annually.

Problem #3: Money Laundering.

Transaction Money Laundering is a form of electronic money laundering that allows illegal merchants to obscure their transactions by processing sales through an approved vendor's payment credentials. While specific estimates may be challenging, various reports and studies provide insights into the scale of global money laundering. These estimates often range from hundreds of billions to trillions of dollars annually.

Let’s take a closer look at E-Commerce as a whole.

Payment Card Providers utilize their centralized Payment network with huge throughput.

But currently adopted payment card schemes involve significant security decentralization through onboarding, authentication, and fraud prevention within Payment networks. Let's dive deeper into each aspect:

Onboarding: Issuing banks manage onboarding cardholders, verifying their identity, and setting credit limits.

Multi-factor authentication (MFA): Payment Networks encourage the use of MFA for online transactions, which often involves verification through independent providers like mobile phone carriers or biometric authentication companies. This decentralizes the authentication process.

Fraud scoring systems: Many banks and payment networks utilize fraud scoring models developed by independent companies. This avoids any single entity having complete control over fraud detection and mitigation.

Financial crime finds a way around security decentralization, fueling crime syndicates and terrorism. The largest economic impact on the E-Merchants is falsely declined sales and fraudulent product reviews causing immediate damage to their bottom line.

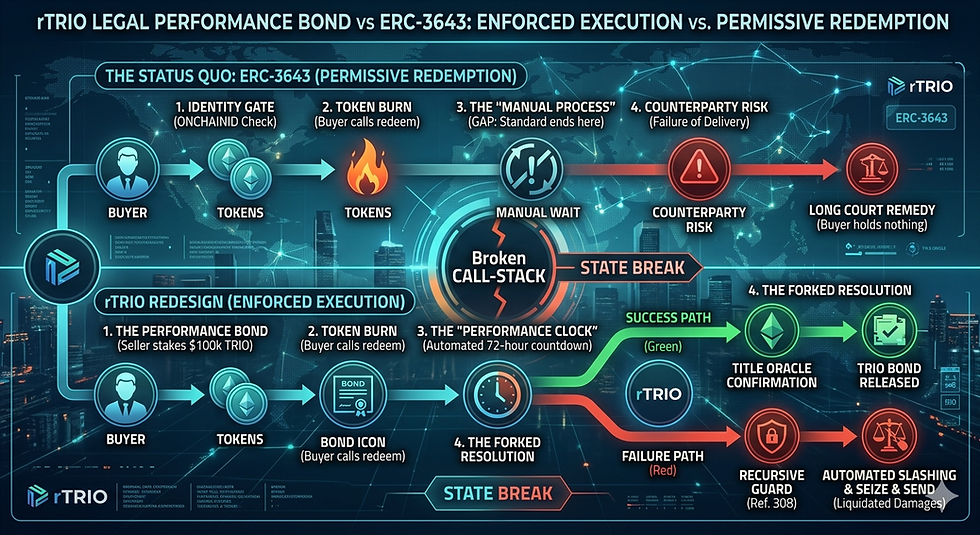

TRIO Identity and Payments network uses a radically different concept. It utilizes a decentralized Payments network built upon a Public Blockchain. But the Security aspects are centralized, including:

Onboarding of Buyers (individuals or businesses) and Sellers (Individuals or businesses),

Strong real-time identification of Buyers and Sellers,

Transactions audit, providing a single map required to prevent transaction money laundering.

This has an important advantage over the existing state of the art. There is a strong synergy between the decentralized Payments network and Centralised Identity-centered, Security, as implemented in TRIO, This synergy is manifested via TRIO Utility Identity Token. This token cannot be transferred outside the TRIO network and it cannot be utilized by anyone outside the TRIO network. Thus the issue of theft is prevented by design. Inside the TRIO network, any transaction proven to be fraudulent can be reversed. Thus the issue of fraud is prevented by design. Since all the transaction data is centralized - it allows the single map to prevent transaction money laundering.

Finally, the ultimate test of the "5-dollar wrench attack" (the crypto equivalent of "your money or your life") will be discussed.

TRIO Identity and Payments network uses a radically different concept. It utilizes a decentralized Payments network built upon a Public Blockchain. But the Security aspects are centralized, including:

Onboarding of Buyers (individuals or businesses) and Sellers (Individuals or businesses),

Strong real-time identification of Buyers and Sellers,

Transactions audit, providing a single map required to prevent transaction money laundering.

This has an important advantage over the existing state of the art. There is a strong synergy between the decentralized Payments network and Centralised Identity-centered Security, as implemented in TRIO. This synergy is manifested via TRIO Utility Identity Token. This token cannot be transferred outside the TRIO network, and it cannot be utilized by anyone outside the TRIO network. Thus the issue of theft is prevented by design. Inside the TRIO network, any transaction proven to be fraudulent can be reversed. Thus the issue of fraud is prevented by design. Since all the transaction data is centralized - it allows the single map to prevent transaction money laundering.

Finally, the ultimate test of the "5-dollar wrench attack" (the crypto equivalent of "your money or your life") will be discussed.

Comments