Tokenised Deposits with the rTRIO Solution.

- id-bound

- Apr 28

- 2 min read

Updated: May 3

🤑 The "Dead Liquidity" Problem in TradFi.

In traditional finance, billions are "trapped" in settlement queues (T+1/T+2) or escrow accounts. This is known as Dead Liquidity—capital that cannot be used elsewhere but has already been committed to a trade. rTRIO eliminates this issue by transforming static balances into Context-Aware Liquidity.

🚀 Mitigating Intraday Liquidity Risk

For an institutional treasurer, rTRIO provides three specific risk-mitigation vectors:

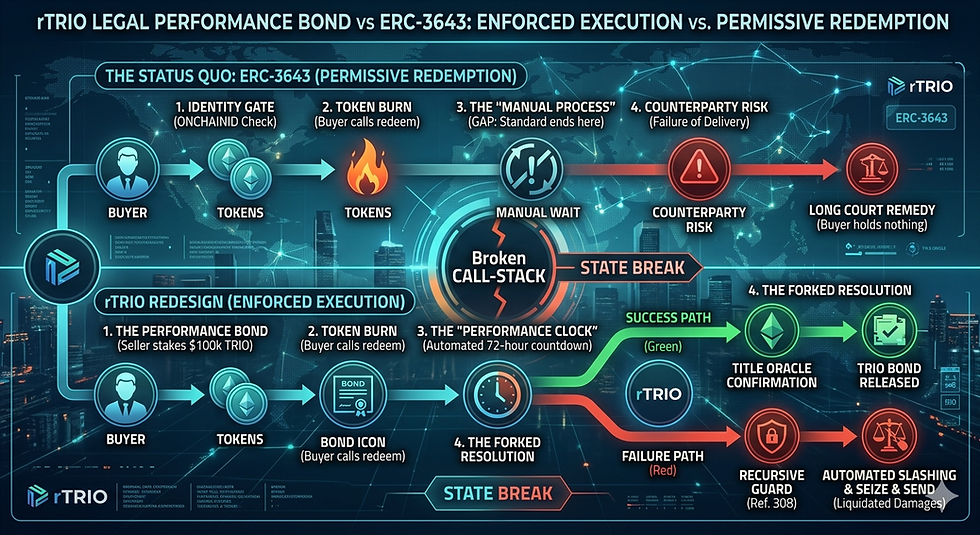

A. Atomic Delivery-versus-Payment (DvP)

The Risk: "Principal Risk"—sending the rTRIO payment but failing to receive the Tokenized Deposit asset.

The rTRIO Solution: If the asset isn't deliverable, the rTRIO doesn't leave the wallet.

B. Reduction of "Gridlock."

The Risk: A chain of settlements fails due to a third party delaying a manual KYC check or title clearance.

The rTRIO Solution: Using rTRIO automates the compliance check. The rTRIO "knows" its destination is cleared before the transaction is even broadcast, preventing "failed trades" from clogging the liquidity pipeline.

C. Just-in-Time (JIT) Funding

The Risk: Keeping large amounts of cash in non-interest-bearing escrow accounts.

The rTRIO Solution: Because rTRIO only pulls funds when all conditions are met, the Buyer can keep their rTRIO in a yield-generating vault or a repo-market contract until the exact second of settlement.

👏 Compliance Framework

Institutions cannot hold "bearer" assets that they cannot control in the event of a court order.

Origin Tracing: Every rTRIO token carries its "KYC-Origin" footprint, enabling "cash-like" behavior in the wild while maintaining a complete audit trail for the Institutional Spender.

🚀 Secondary market for retail investors. Huge liquidity booster.

👏 Strategic Conclusion

The rTRIO architecture is the first implementation of Conditional Liquidity that satisfies the "Basle III" requirements for intraday monitoring and the "MiCA/SEC" requirements for programmable compliance. It moves the financial industry from a "Trust, then Verify" model to a "Verify, then Move" model.

🪙 In layman's terms: anyone can legitimately buy, 24/7, the interest-bearing Bank's tokenized deposit (or any other Real-World-Asset) and legitimately trade them, 24/7, with anyone else.

Comments